The economic world has been in a state of flux over the last 12 months with significant changes in both product prices and the cost of production.

In the agriculture sector it has been no different with large cost increases in FY 22, but correspondingly large lifts in product prices as well. You can see a bit more about the FY 22 year in review from our own dataset in this article.

In FY 22, we extracted actual data from our New Zealand wide customer database which showed operating costs had a significant lift from the year before of around 15%, well above the NZ CPI rate for the same period of 6.9%.

But that change in cost didn’t stop at the end of FY 22.

This week, we’ve surveyed our Client Directors across New Zealand to see where their customer budgets are landing for FY 23. As you might expect, that range is relatively significant, from $5 per KgMS to $7.20. However, the average is landing at $6.25 per KgMS before depreciation.

So whilst the dairy sector is “enjoying” record payouts, the devil, as they say, is very much in the detail.

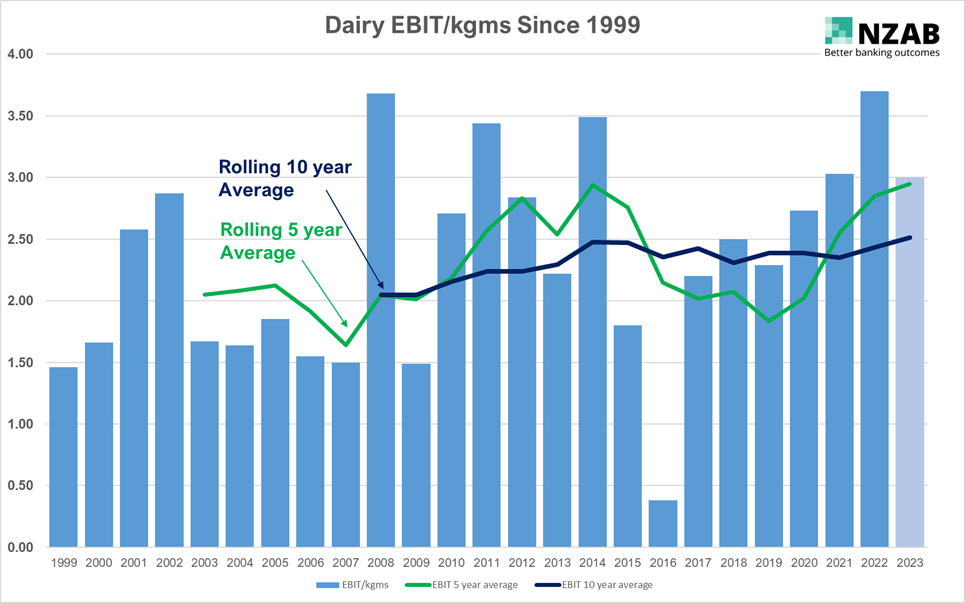

To add some further data to this anecdote, we’ve put together the graph below which examines how dairy EBIT per KgMS has been trending over the last 20+ years. The data is sourced from Dairy NZ’s economic data since 1999 to 2021. For FY 22 we’ve used our own data set and for FY 23 we’ve used a $9 cashflow payout less our surveyed average cost of $6.25 above (plus an allowance for depreciation).