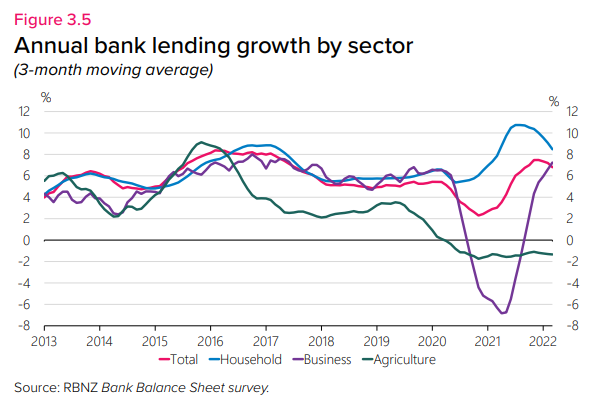

In our last article, we talked about the evident return of bank credit appetite in the Agriculture sector, a welcome development for farmers as capital availability is important for both increasing productivity and confidence in the sector. Both are good things, and they encourage further investment plus ensure that talent is attracted to the sector, critical for future success.

In this article, Scott Wishart and I came together to collaborate on a new article to broaden the discussion and talk about the observed credit cycle in agriculture – what causes it and what to look for.

This is important to understand as these cycles are much shorter than the investment period of a farming business. In other words, it’s not uncommon to see less than 3-5 years from peak to the trough of a credit cycle - yet the investment in farming is generational and needs to outlive both the top and the bottom of these peaks.

The causes are not always the same either. Sometimes it’s due to the lack of sustained profitability in the sector, other times it might be a generalised credit crunch. Sometimes like we saw in 2016 onwards, it was increased regulatory capital requirements making agriculture loans less profitable.

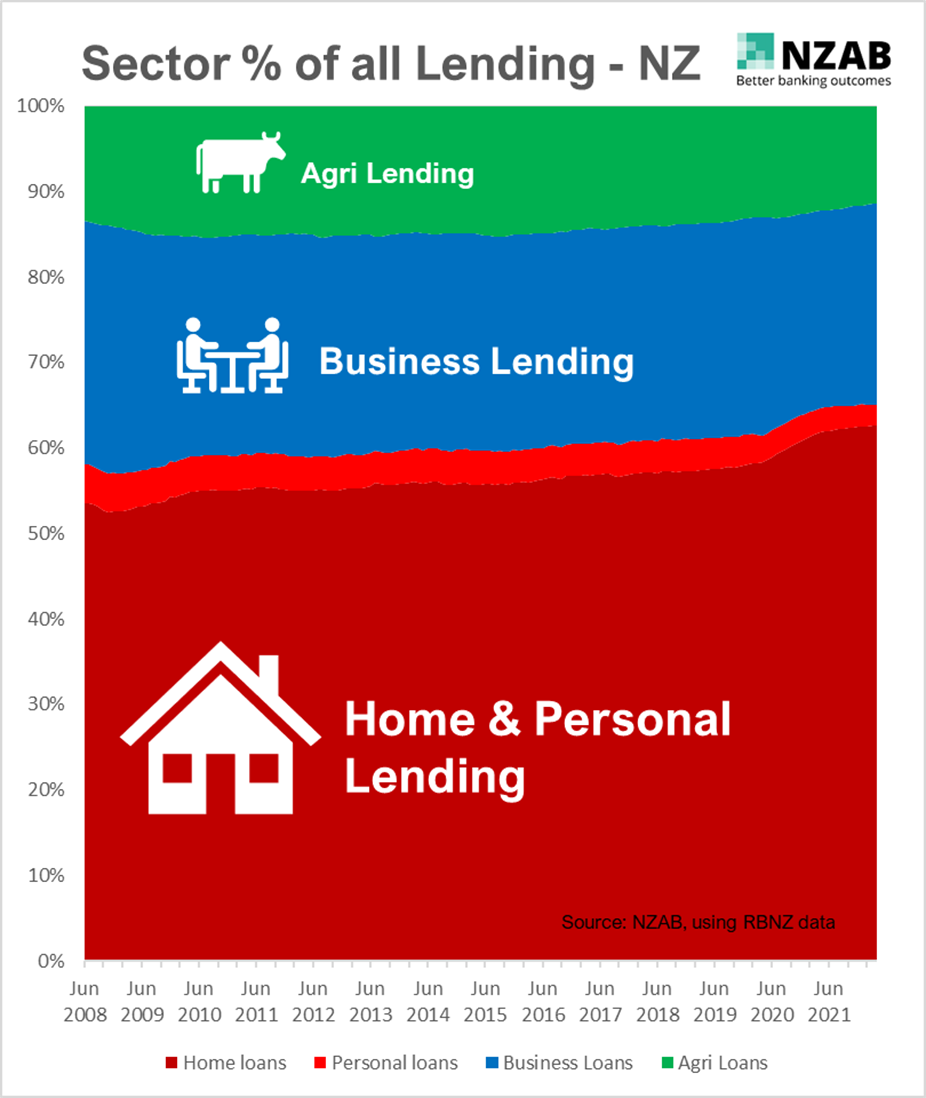

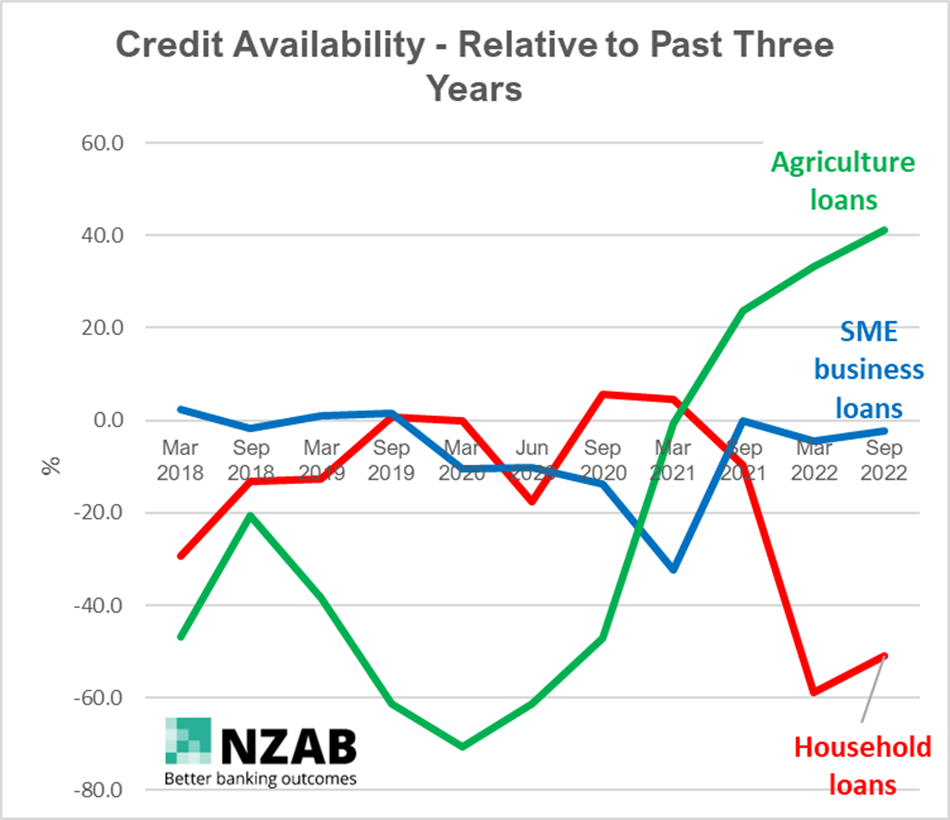

In other times it’s sector weighting versus other sectors in that bank, or even at the parent bank. An example of this that we’re seeing playing out right now is where one sector (housing) is becoming “full” for the bank and where another sector (agriculture) has loans that are getting repaid faster than they are growing creating a positive supply gap of credit.

Learning how to spot the early signs of change and what drives these changes is critical when making your investment decisions. Sticking to rigorous behaviours with business management and decisioning is key.

The cycle can be best represented by a sine wave as follows: