Recent Posts

Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

With the ongoing Inquiry into Rural Lending, one of the central themes from both the RBNZ and the Banks is that Agri Lending is ‘riskier’ than Home Loans so therefore a higher margin needs to be charged to justify the lending.

Two things have now happened over the last 10 years. Firstly, the Banks have increased the price of their loans, but perhaps more importantly they have also reduced the risk they take at the same time.

Let’s unpack that statement a bit more.

A Bank considers two main factors when looking at a loan. Firstly, what is the likelihood that things will go wrong (i.e. default) and secondly, how much of the loan that they will be able to get back if things do go wrong. When a loan does go wrong, the Bank assesses how much they might lose on the loan, and this is referred to as a ‘credit impairment allowance’ or an ‘individual provision’.

Now, it’s very important to note that an individual provision (an ‘IP’) doesn’t necessarily turn into an actual loss, the Bank just thinks it might.

From experience, banks prefer to budget or ‘provision’ a higher number than they actually do lose, as they don’t like surprises.

Banks don’t publicly report the actual losses they make so we can only use the IP data as a proxy for this detail. However, it was telling when Antonia Watson, CEO of ANZ, was asked at the banking inquiry how many defaults they were running in their Agri loan book. Her answer - “Just two” – in over $15bn of loans.

So, let’s look at the data. The graph below shows the level of total annual bank Agri IP’s (Main banks + Rabobank + Heartland) as a percentage of their total advances since 2018.

Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

When we made our submission to the Rural Banking Inquiry, we went back into the RBNZ data to look at how each main banks' Agri Lending market share has changed over the last six years.

The changes in market share are really telling, but what’s more interesting is the actual dollars that have been lent (or as the case might be, haven’t been lent) when looking at other sectors such as home lending.

Let’s look at the graph of the market share first:

Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

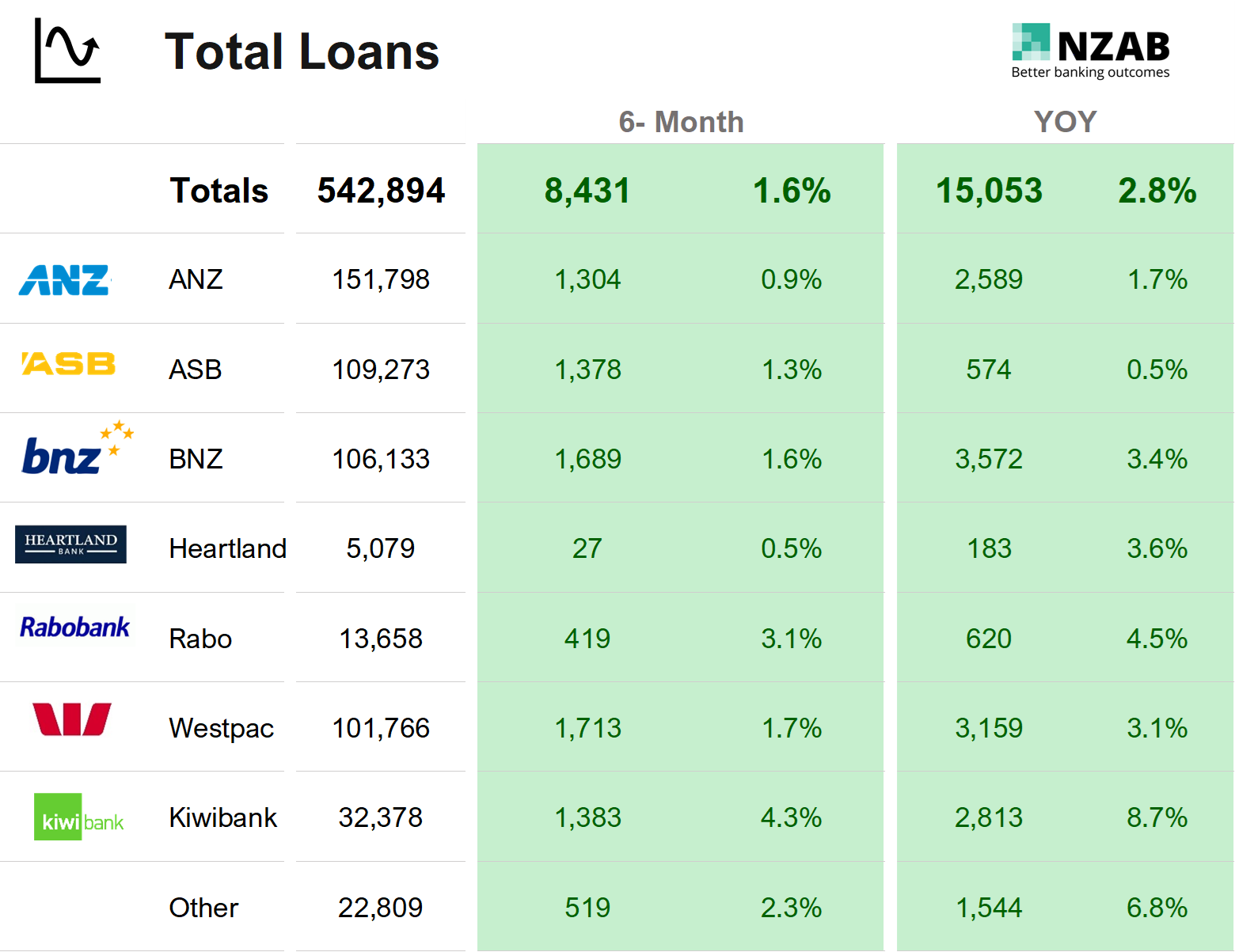

We’ve dived back into the RBNZ data to see all the main bank movements over the last six months- all the changes in lending, who’s winning market share and who’s losing it- in both the Agri and Business Lending Sectors.

In this Issue:

- Whilst the growth in total loans continues for all NZ banks, it remains quite anemic, a continuation of the slowing in credit growth that started in late 2022, but huge overall growth for Kiwibank with 8.7% growth

- Westpac Agri lending is lagging the other banks, (even ANZ, who continues to drop) with its' Agri loans reducing by $350m for the year, resulting in a market share drop of 60bps. Rabobank was again the benefactor, picking up 75bps of market share.

- ANZ shed a whopping $1.6bn in business sector loans over the last 12 months - one of the biggest retractions in lending over a period we've seen. ANZ now has less business loans than what they had in 2020, and over $2bn less in Agri loans, However, during this time, they have increased their home lending by almost $20bn

- Dairy loans continue their ongoing repayment profile, reducing by over $500m for the year, going some way to explaining the strong demand for loans in this sector.

- Horticulture loans continue to grow substantially, up a further 8% for the year despite Agri loan growth being largely flat.

- Agri non-perfoming loans and lending provisions were largely flat over the year - this is likely to be the balancing of risk between an improving dairy situation, but a sheep and beef sector that remains under pressure. Additionally, the viticulture sector was under some earlier concerns which has now alleviated somewhat, similar to that in the Kiwifruit sector

As always, please sing out if you have any questions or would like to use the data in your own presentations or engagement with customers. We would be happy to provide a digital version for sending.

Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

We first started talking about Kiwibank being re-purposed for Agri growth (and more business lending) in this article here

Within that article we discussed Kiwibank’s success, but despite that, capital regulations were preventing them from becoming a meaningful player in Agri lending.

Quite simply, Kiwibank has a limited amount of its own equity capital, and the capital adequacy rules (i.e how much of its own equity it needs to place against each loan) means that it’s more incentivised to lend on houses than it is to an Agri or business customer.

Now, the future of Kiwibank is again on the table after a speech by Nicola Willis, New Zealand’s Finance Minister, over the weekend. One of the ideas circling parliament at the moment is to expand Kiwibank by allowing it to seek more capital - this might be either from Government itself, or further external capital. The earlier Commerce Commission report on the banking sector actively supported the expansion of Kiwibank as a way of encouraging further competition in the New Zealand banking sector, so any move from Government is likely to be on point with this.

The only trouble with that approach, is without any change to capital regulation, any non-specific capital introduction into Kiwibank is more than likely going to simply stimulate a further expansion in home lending credit – great for home owners getting access to competitive credit (and also for house values) - but absolutely no use whatsoever to the productive sector.

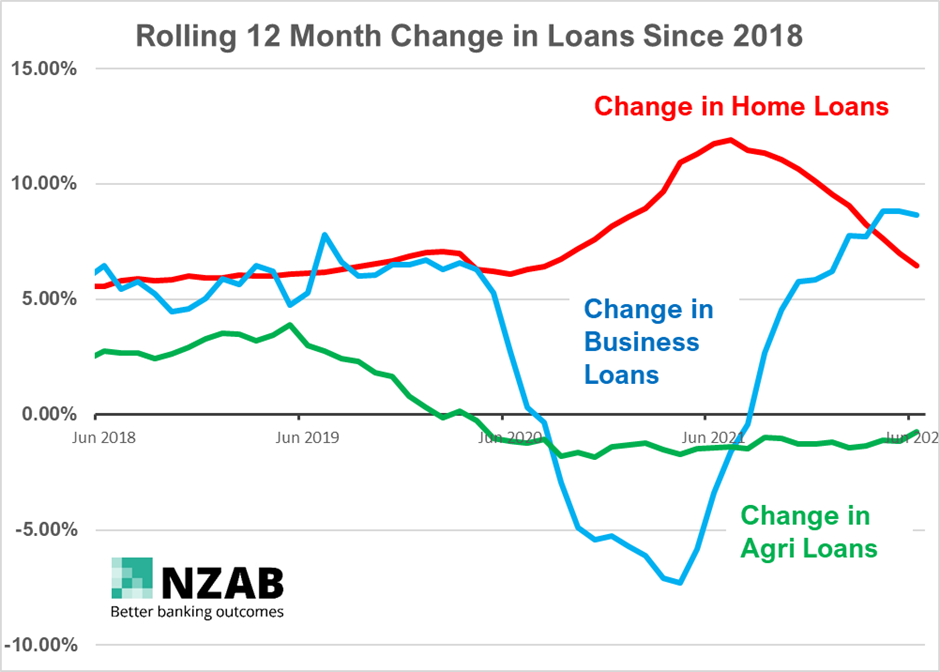

We saw a version of this during Covid – when the RBNZ introduced the LSAP programme, they provided c. $50bn to New Zealand banks as lines of additional credit. When added to the government’s own stimulus we observed a huge amount of additional liquidity landing in banks. In turn, given their capital settings favoured home lending, the banks did what they did best and fed it down that channel - leading to a significant explosion in home lending, subsequently fueling house price growth.

If you prefer to see this more graphically, the below graph shows that bulge of new lending going through:

Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

With the official announcement from the NZ government about launching an inquiry into Rural banking, we believe it’s an opportune time to share NZAB’s thinking on solutions that would increase the availability of competitive capital to farmers.

In our last article, we shared our submission to the Primary Production Select Committee. We were subsequently invited to present directly to the committee in person alongside Federated farmers and Rural Women’s Network.

In that submission, we outlined the problems we saw and the reasons behind them. We purposely stayed away from offering any solutions as we thought it was best to focus on identifying the issues first.

But now, we thought it worthwhile to share some of our thinking on what would increase both the availability of capital and the competitiveness of it.

In this article, we will touch on changes to “capital regulations” as one solution, but we will also touch on another five things that need to be focused on at the same time. The current capital restrictions that farmers' face is a problem due to multiple factors, not just the current bank settings.

Equally, changing capital regulations alone won’t solve farmers access to capital – it's only part of the puzzle. And it’s inherently risky if farmers' only focus on one area (capital regulatory change) and put all their eggs in that basket only to find that the RBNZ is unwilling to change.

The prize here is large.

Make no mistake about it - capital restriction due to regulation causes market harm. In the case of Agri, it can lower a farmer’s confidence in investment and even when investment is chosen, it drives up the cost of the capital deployed with it. It also sends the market the wrong signals, leading to asset price suppression, even when the underlying operating performance of the asset class is doing well.

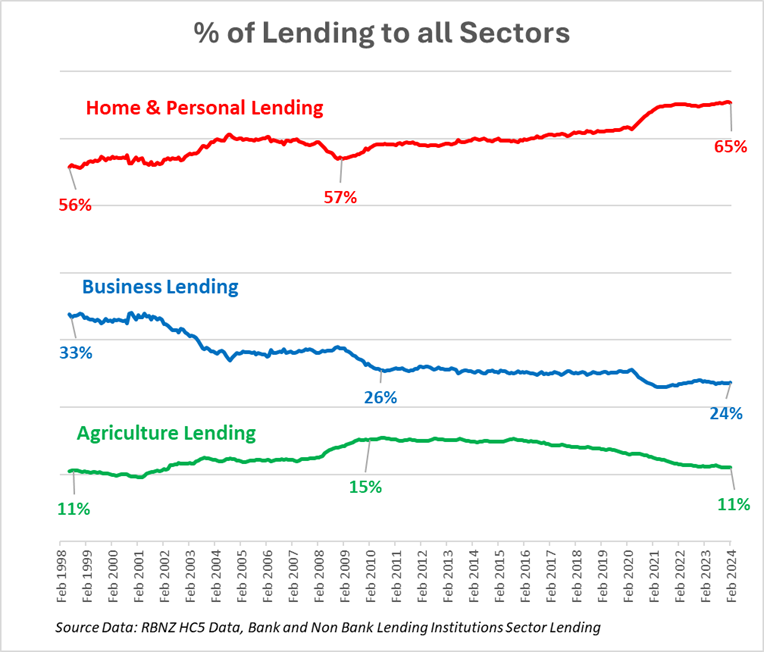

Conversely, as we’ve seen in the home loan sector, it does the opposite – not just funnelling more debt capital into houses, but also investment capital as investors know they’re on a one way bet with rising asset values.

This regulation is creating bubble and bust situations with the classic case being the New Zealand housing market.

However, get the regulations right and capital will follow the right economics, rewarding those investments that have good economic returns and strong market fundamentals, consistent over a long period of time.

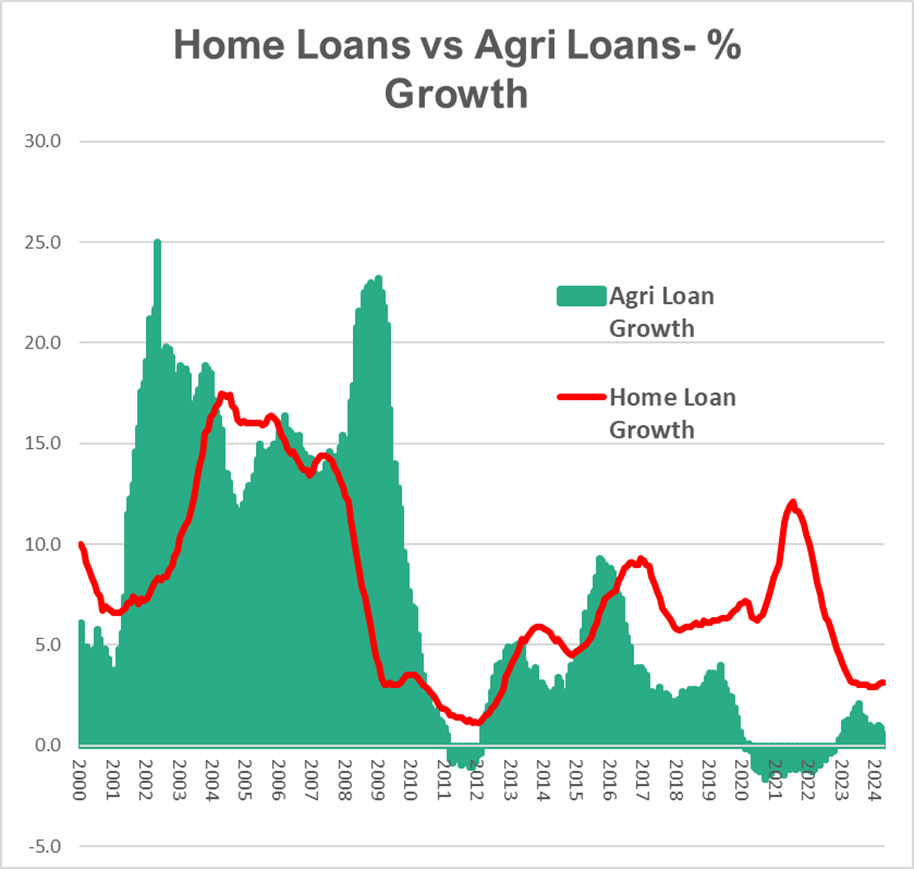

Let’s start with a picture.

As always, we want to start with a graph to paint the picture.

The below graph is the year-on-year percentage growth for Agri Loans, versus Home loans, dating back to 2000.

The point of this graph is to remind everyone that it was commonplace for Agri to have equal access (versus other sectors) to credit. Up until 2016, Agri lending growth closely followed the cyclical nature of all lending in New Zealand, but subsequent to that, you can see the clear re-direction of bank lending towards Home Loans.

New Zealand Agri Brokers Limited (NZAB) was recently invited to make a submission to the Primary Production Committee on Rural Lending. This is a New Zealand government select committee chaired by MP Mark Cameron.

The committee opened a briefing (not a full-scale inquiry) into this topic as they had received widespread feedback from farmers and other industry participants about the apparent disparity between rural and urban bank lending practices. They are initially seeking to gain a better understanding of the nature of the problem before working out any next steps.

NZAB made the following submission and as this is a public process, we thought it would be useful to share our submission with our wider farming and farm professionals’ audience.

If you have any question on any part of our submission, please feel free to contact us.

Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

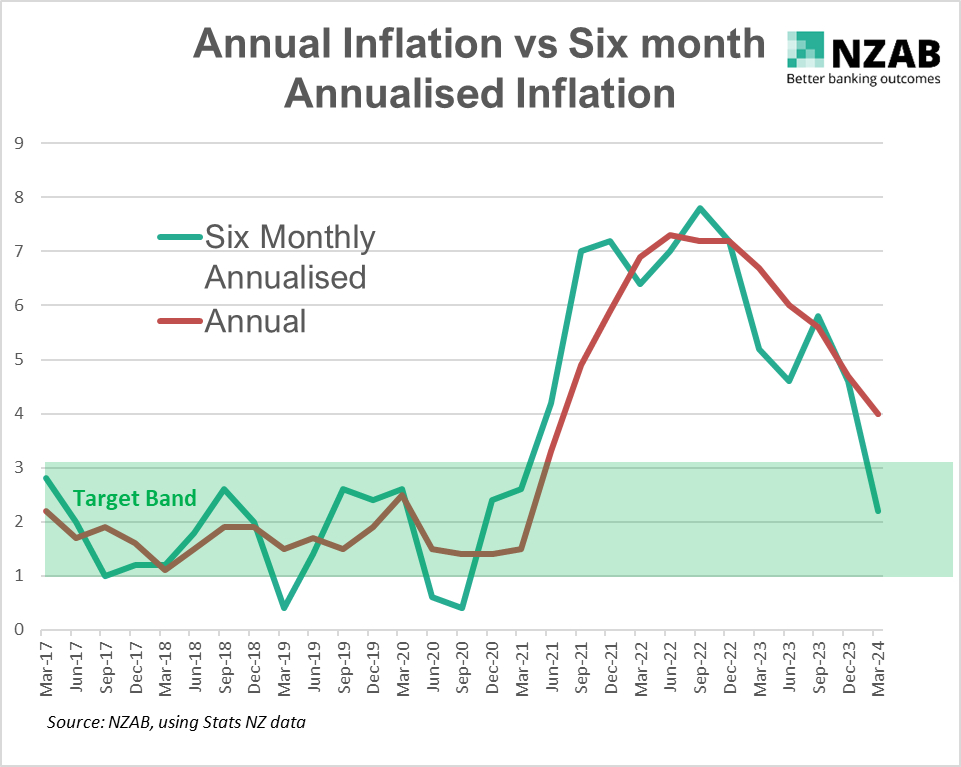

The recent CPI release of 4.0% for the year ended 31 March 2024 was a step in the right direction, falling further again from the December number of 4.7%. It arrived in line with economists’ consensus levels and slightly higher than what the RBNZ thought (3.8%).

But it was still noticeably above the ‘accepted’ 1-3% target range.

Consequently, the RBNZ let all parties know it, with a brief statement noting that the “OCR needed to remain at restrictive levels for a sustained period”. Also unhelpful was that despite ’tradable inflation’ printing at 1.6% p.a., non-tradable inflation was 5.8% p.a. (more on this at the end of the article) leading most economists to say “we need to be here longer” and pushing out rate cut forecasts further into 2025.

But are we yet again being over obsessed with looking backwards rather than looking at what’s happening right now?

Let us explain. The latest CPI print of 4.0% is made up of 4 quarters - and they look like this:

Quarter ending June 2023: 1.1%

Quarter ending September 2023: 1.8%

Quarter ending December 2023: 0.5%

Quarter ending March 202424: 0.6%

Total equals 4.0% for the year

So, what if we extrapolated forward the last six months of CPI change and annualised this to the rest of the year?

Well, we would get a 2.2% inflation rate, being (0.5%+0.6%) x 2 which is smack bang in the middle of our target range.

The graph below shows it best by plotting the six-month annualised figure against the annual figure since 2017.

Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

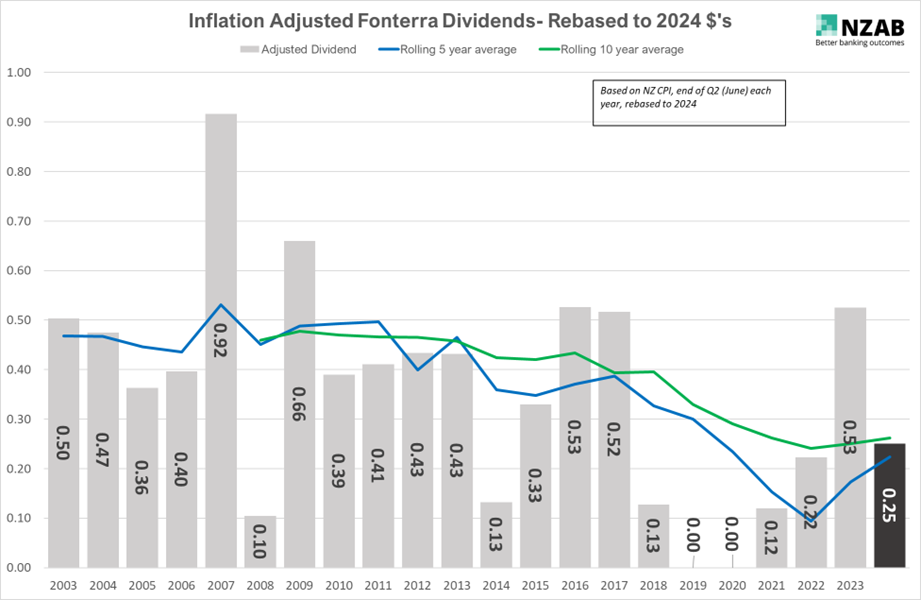

We’ve been through (and arguably are still going through) a period of pretty ugly inflation in New Zealand. Inflation has impacted on all sectors of our economy. but farming felt it more keenly being exposed to some big increases in wages, fertiliser and fuel.

So, given the changes in inflation, what does a good milk payout now look like?

With many farmers looking to make investment decisions and also considering hedging policies, we thought it might be useful to put out a few graphs showing the difference between inflation and non inflation adjusted payout data over the last 20 years to assist.