Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

With our clients we’re always in a continuous budget setting and forecasting mode so we can try and stay well ahead of what might happen and what impact it might have on key decisions. This can include debt repayment, capex projects, expansion feasibility and working capital facility management.

It would be fair to say that the last six months have been very difficult with significant downwardly revised income projections and costs still remaining sticky (and even increasing) on the back of inflation spiraling.

Going into FY 24, this is not going to get easier with a wide range of milk payout, meat and crop price expectations in the marketplace and rapidly changing macro events that may or may not flow through to on-farm input and capital costs.

With that intro out of the way, the following are some key thoughts as we move through the budgeting phase for FY 24.

First, what milk payout should we use?

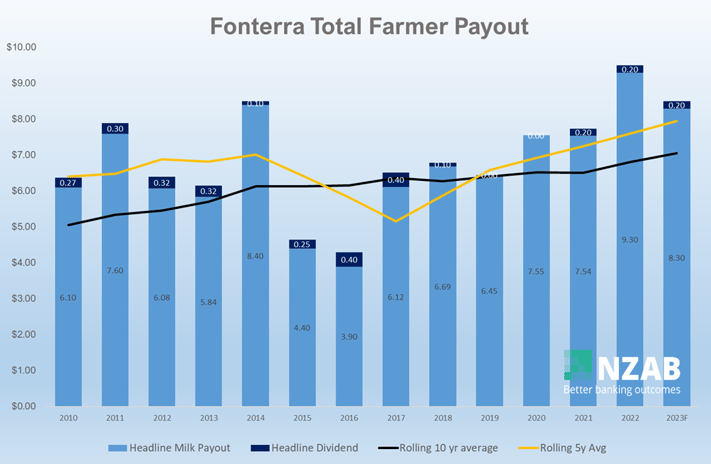

First of all, some data. Below is Fonterra payout, since 2010 with dividend on top. The yellow line is the five-year average, and the dark line is the ten year average.

The ten-year average, whilst the best ever at $7.05 (6.87 Milk plus 0.19 div.) looks a bit sick in context of the last two years. Given the vast inflationary period we’ve faced over the last period, the five year $7.95 ($7.83 plus 0.12 div) is a slightly better representation of what mid-term “status quo” projections should be tied to, but we’re still a bit indifferent to whether that accurately reflects the changed inflationary world we have been through over the last two years.

Looking more closely at actual market data for milk, a bundle of milk commodities sold now, less processing costs would suggest about $7.40-$7.70 at current pricing. Last year when I wrote a similar article it was north of $10. Jeepers.

Milk hedging for FY 24 suggests a payout of $8.25 at the time of writing. Obviously, prices would have to increase from here to achieve that.

So, what to use for his year’s budget? The answer is not straightforward, but something around $7.50 to $8.25 would be prudent as a starting point.

Keeping in mind that deferred payments from FY 23 will be getting close to near certainty based off processor forecasts. This really means we’re just estimating what the advance to next May (2024) will be, at $7.50, this would be c.$6.00. At $8.25, that’s about $6.60 like this year.

All of the above said, I would be running another version of your budget at $7.00 (or even less if you prefer) to see the impact. More on this below.

It’s important to note that this isn’t an estimate of what we think the payout will be for FY 24.

That’s a mugs game to try and pick that.

Even amongst the bank’s economists we observe a range of $7-10 -that’s massive! It’s clear in both New Zealand and around the world we are in an economic “no man’s land” with wide ranging views about recession, inflation and economic turnaround. Even the most learned punter could make a case for milk payout going up or down from here.

What is important, is making sure that your financial forecasts allow you to make good and confident decisions around operational planning, capex decisions, and stakeholder management.

That last one – ‘Stakeholder management’ is typically going to be your bank and your governance team. Presenting a budget to your bank and governance team that you have confidence in meeting is critically important for relationship stability. Let’s say that again – “confidence in achieving”. It should not be “we hope it lands here”.

“Hope” when it comes to a higher payout is not a great strategy.

“Hope” when it comes to lowering costs or unachieved production is not good either.

This might mean that the budget you present is barely breakeven or worse in the first cut.

However, it takes courage and clear articulation (supported by good mid-term strategy) to present this and very good communication to ensure that your stakeholders don’t panic.

The margins in FY22 were very good – maybe the best yet. FY 23 margins were tight but not disastrous. FY 24 at a low $7 payout (if that were to occur) will be very challenging indeed.

But the point is that farming is always like this- it has some years with great margins and some years that are an absolute dog. Farming is a long-term game and the key for both farmers and banks is that neither side should panic at times of low profitability. Just like we shouldn’t lose our heads in times of high margin.

Banks do know this but presenting or reminding them of this is not a bad idea either. At the very least, you’re demonstrating your strategic thinking and governance depth with managing volatility.

So, if the first cut of this year’s budget looks a bit sick it’s not a time to throw the baby out with the bathwater and re-design your entire operating system. We have seen periods like this before and need to ensure both farmers and banks alike take a mid-term view with these periods. To support this mid-term thinking, presenting historical, current and future projections (beyond FY 24 and even an “SQ budget”) would be a smart thing to do.

None of the above means that you shouldn’t be aspirational with your management team about achieving even higher production or even lower costs – but don’t build that outperformance into your stakeholder budget unless you know you can absolutely deliver it.

That said, during time of low margins, attention to detail becomes very important, so from a cost management and planning perspective, consider a few of the following budgeting “must dos”:

- Go line by line, unit by unit. An example here is fertiliser. Prices are falling rapidly here so know what you are applying and when. Some fert companies also put out forecast expected prices into the next 12 months so you can very accurately work out when and how much this will cost from a cashflow perspective. You might consider sensitising at different prices too if you’re a big user.

- Know your resource base. This is your feed supply and demand budget including your feed inventories. Be very real with the planning on this (not aspirational to a level that hasn’t been achieved before) and monitor regularly.

- Continually review the budget – this goes for pre-budget setting and post budget re-forecasting. It’s got to be dynamic based on the most recent information to hand. Same goes for peer review, share amongst your advisors and even your peers for insight.

- Don’t get excited/panic when Fonterra releases its opening forecast. I don’t need to tell you all here how different an opening forecast and eventual payout will be. Likewise, don’t immediately adopt what they put out into your budget.

- Remember the Fonterra super dividend this year. For Fonterra shareholders this might be one of the timelier cashflow lumps we’ve had for a while. 50-70 cents is expected plus the normal operating dividend on top.

- Set the right culture from the top. Without being overzealous, drive good cost management from a governance level. Emulate what good cost control looks like with examples to your team. There’s a balance here though- too far and fear takes over which can lead to sub-optimal operating systems being adopted and stress building – find the right balance here.

- Cash is king. Have facilities ready for the worst-case result. What working capital facilities do you have in place and what buffer is available within them? What does it look like at very low payout levels? Are they still adequate? Engaging with your bank for more facilities at short notice because payout levels have fallen dramatically is risky versus having these already in place when times are better. Don’t be in the queue with others when things are at their worst. Know what the worse case looks like and have those facilities ready to go if needed. Think about how confident you will feel right now, knowing that you have the “downside” already planned for.

- If there is buffer in the budget for further capex and debt repayment, make sure it’s not all front loaded – structure as much as you can towards the end of the year when more is known about the years profitability levels.

- Consider hedging strategies. This is equally relevant at low or high payouts but don’t be knee jerk with decision making here. Have a clear and enduring policy that considers all risks in the business. Understand clearly the differing profit levels at differing payout levels and don’t consider milk price hedging in isolation to the other costs of business and/or other risk mitigants. Remember farming is a cyclical beast that delivers consistent average prices when looking in longer term cycles of five years plus.

These are a few tips to consider when you go through the budgeting process, and we’d love to hear your other bits of advice that have served you well over the years.

Last of all, make sure you have a great advisory team around you as you navigate the times ahead.

Having the confidence to act during times of uncertainty has proven to be one of the more powerful wealth creation/preservation actions you can possess. Make sure you have people in your team that can deliver that for you.

Contact one of our experienced team on 0800 NZAB12 or click here to send us an email for an introductory chat. We’d be delighted to help you through his process.

Who is NZAB?

Farming’s very complex and you can’t be an expert in everything. That’s why the best farmers gather a specialist team around them. Our specialty is better banking outcomes for our clients.

There’s no one better to work alongside you and your bank. With a deep understanding of your operation and our considerable banking expertise, we can give you the confidence and control to do what you do best.

We’ve been operating for over five years now and we’re right across New Zealand, For an introductory no cost chat, pick up the phone and talk directly to one of our specialists on 0800 NZAB 12.

Or if you prefer, Visit us at our website or email us directly on info@nzab.co.nz