I love cause and effect. Squeeze a balloon and it will pop out somewhere else. Squeeze it enough and it will pop.

Banking is a bit like that at the moment, but for once in a long time, Agri may be set to benefit.

As you all know there’s heaps of noise about the housing market going up, lots of investor frenzy and yet again the purchase of the ubiquitous family home seems to be getting further out of reach for more families.

Its political dynamite – a hugely populist issue and one that the current Government seems determined to solve.

Why do they need to make changes and step this up a gear? “It’s the capital, stupid”

The Government has chucked a few traditional things at it (LVR restrictions) and ruled out a few others (capital gains tax), but they aren’t really working. They haven’t in other countries either. That’s because it doesn’t actually address the underlying issue - How ridiculously easy capital is available from banks in the home loan sector. As we say in the office - “It’s the capital, stupid”.

Big picture for a moment, there was massive stimulus last year with the RBNZ supporting the availability of capital to both Government and the Banks by continually expanding its Large-Scale Asset Purchasing (LSAP) to over $100bn (effectively printing money).

A fair chunk of this money has found its way into the banking sector and the banking sector’s regulations and corporate profitability models are highly stimulative toward home lending. This is simply because:

- Its much easier to originate and serve a home loan (paint by numbers for credit departments and once set-in place, they don’t need much review) AND;

- RBNZ capital regulations mean a home loan is over 100% more profitable (at the same margin) than one to Agri or Business.

But is all that set to change?

There’s some big sound bites coming from this Government at present. Take these from Grant Robertson:

“We want to tilt the balance towards first home buyers while also incentivising more investment into the construction of homes”

“We all know that building more houses, particularly affordable housing is critical, but we can also do more to manage demand, particularly from those who are speculating”.

“It is the time for bold action. The market has moved quickly and rapidly in a way that is not sustainable – we have to confront some tough decisions and we will do that”

Now some of that will be referring to the upcoming changes in the RMA. But make no mistake, he’s about to make it way tougher to invest into housing (if you’re an investor purchasing existing homes).

Bank’s are feeling it too. They’ve become a lot more sensitive to the social impacts of lending. They don’t want to be seen to be encouraging the property market (via increased capital availability) to take it out of reach of family homeowners.

So here are some new ways that we could see the Government influencing this, aside from more LVR restrictions:

- The Big Kahuna:

The RBNZ introduces (directed by Government) a second RBNZ amendment act – changing the mandate of the bank to include housing affordability alongside monetary policy and full sustainable employment.

To actually implement that, the RBNZ would then immediately increase the RWA (Risk Weighted Assets) requirements for banks’ lending to investor rental properties. In short, it requires the banks to hold more capital against these loans making them less profitable.

Cue much higher interest rates for these loans as banks find them less profitable.

- Make interest payments on housing investments non-tax deductible (excluding new builds).

I can hear the cries of “this makes no economic sense” straight away but the Government won’t care. And they did it in the UK in 2017 to stifle property investment.

This would immediately make housing less attractive.

Incidentally, it’s not as bad as it sounds (net impact might by about 1-2% reduction in cash yield), but this will put the frighteners up the investor market. I would still expect new builds to be exempt from this.

And why is this good for Agri?

Well, the amount of capital in the banking system is not reducing.

Think of that balloon again – you squeeze one area, its going to pop out somewhere else. Make some parts of the lending sector less profitable for banks and they will examine the profitability of other parts of their portfolio more favorably.

Agri is one of them.

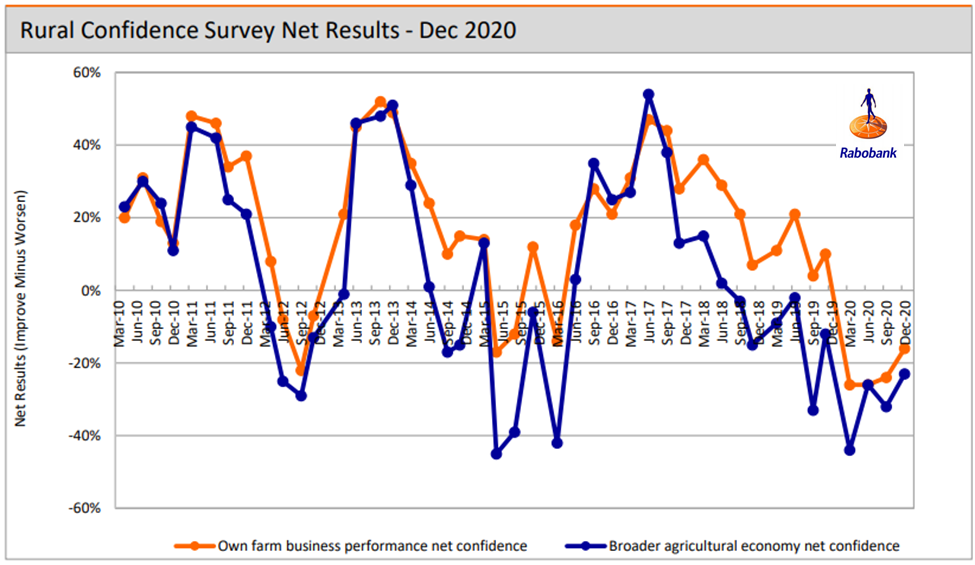

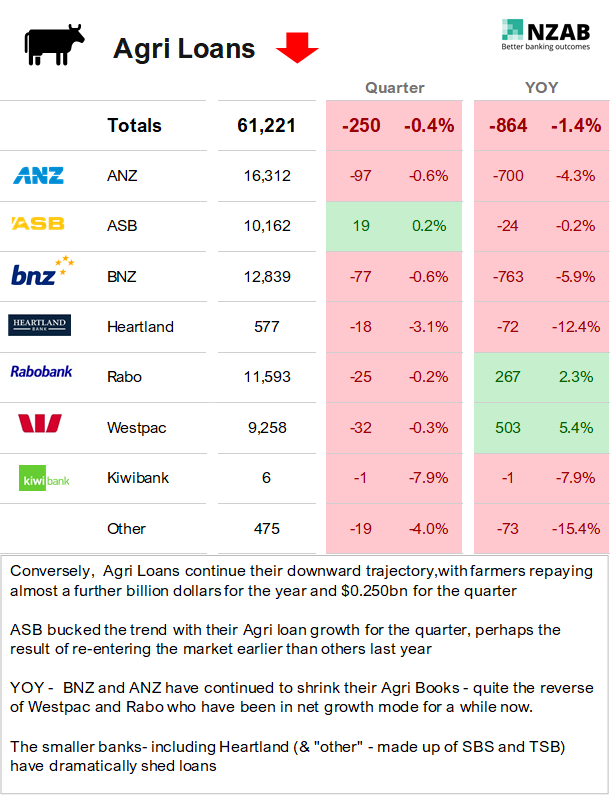

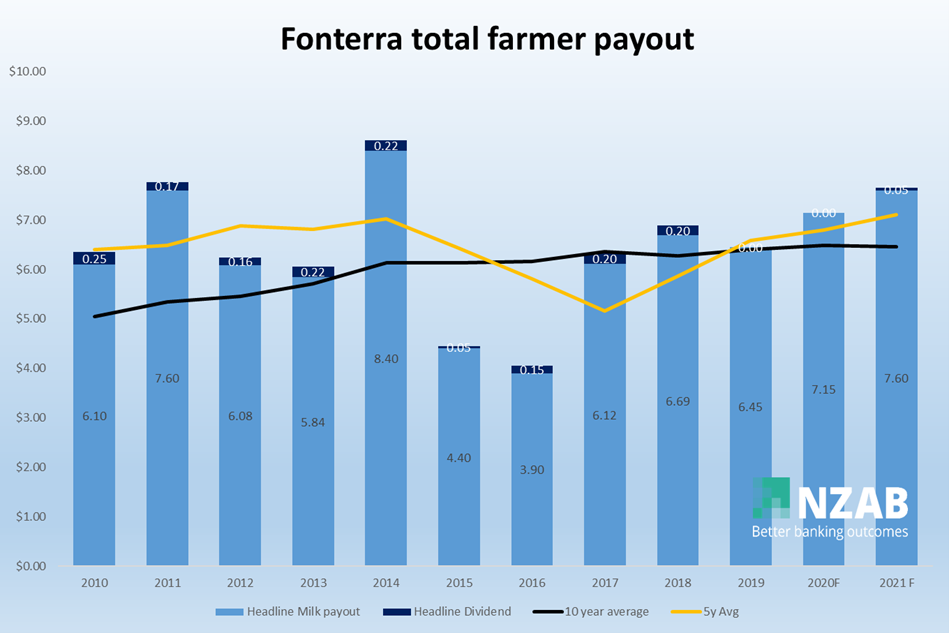

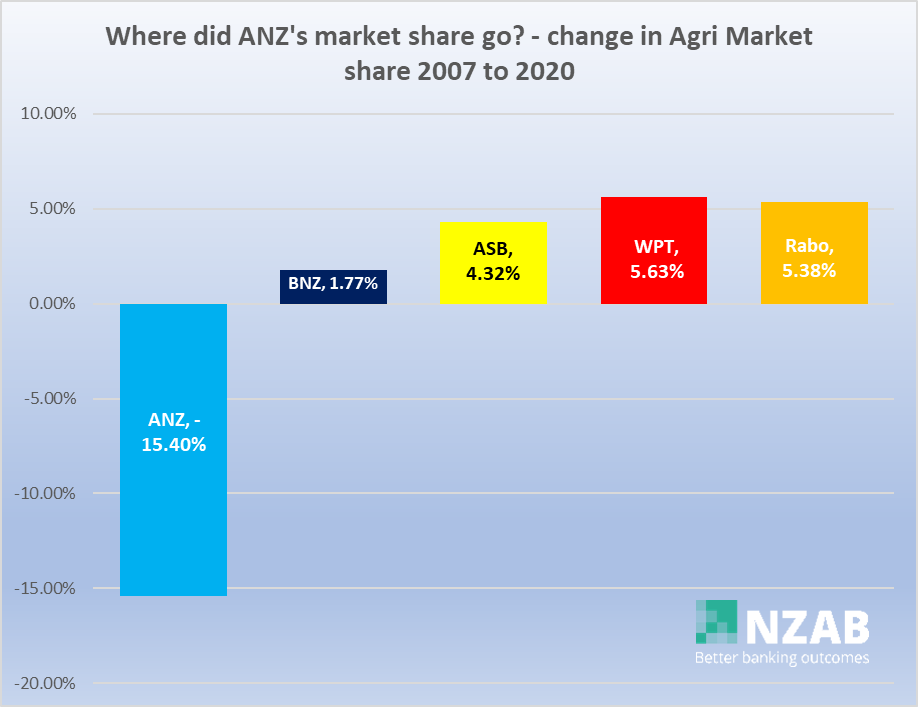

Scale is important here - take the below graph showing the change in lending in both Agri and Housing over the last 12 months