Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

A few weeks ago, we announced the launch of NZAB Capital and our new $500 million agricultural lending platform. At the time of launch, approximately $30 million of loans had already been drawn.

Only a short time later, that number has now grown to more than $80 million of lending either drawn or committed.

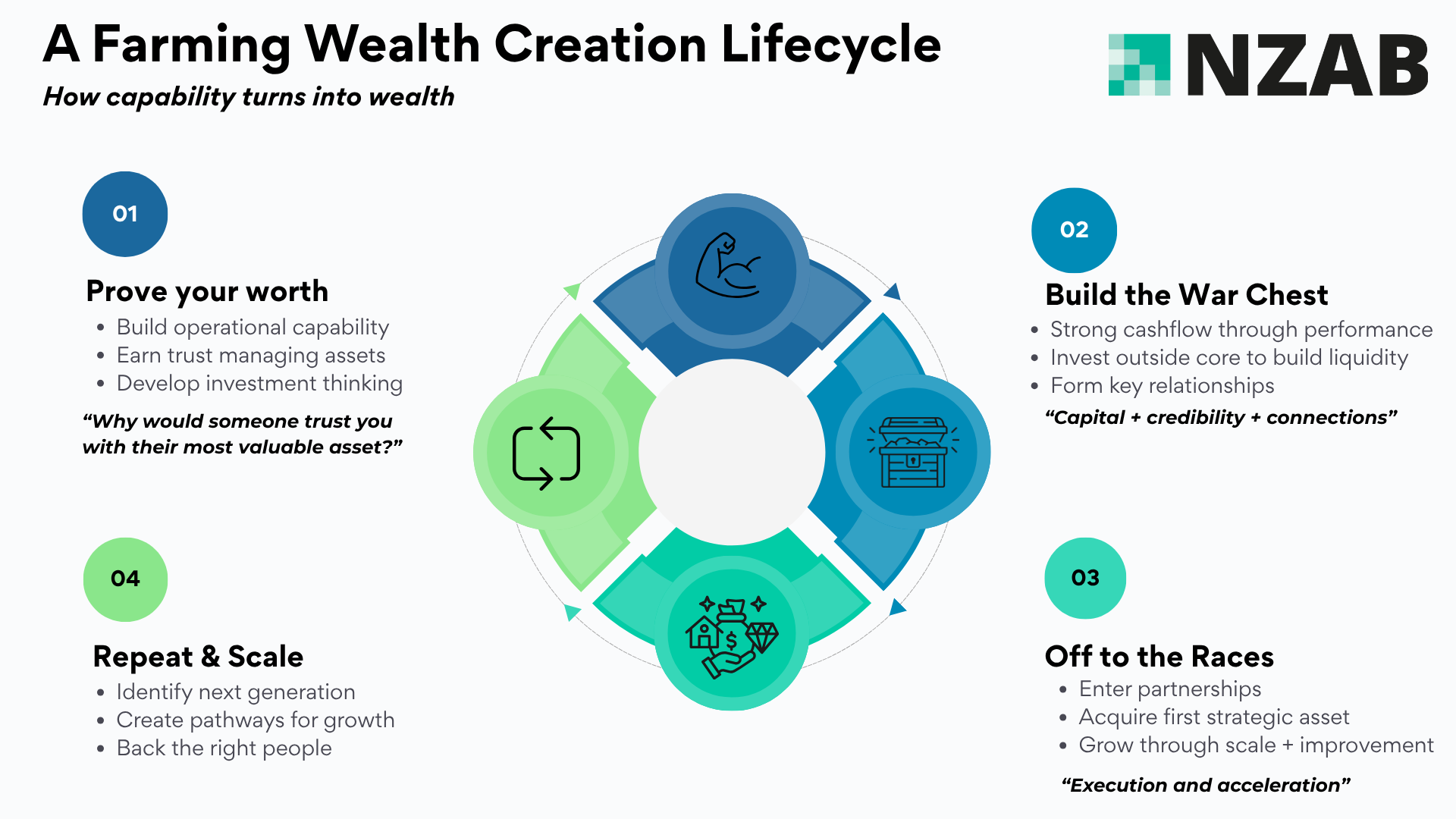

While NZAB Capital is an exciting new part of our business, it is important to reinforce that NZAB’s core business remains advisory led.

For nearly a decade, NZAB has worked alongside farming businesses across banking, debt structuring, succession, growth, governance, capital structuring, acquisitions, and long term strategic planning. A significant part of what we do every day is still helping farmers improve outcomes with traditional main bank funding through better structuring, stronger presentation, and clearer strategic alignment.

In fact, one of the interesting things we’ve already seen since launching NZAB Capital is that some situations initially presented to us as “non bank lending opportunities” have actually ended up back with a main bank once the strategy and structure were better aligned.

That remains a very important part of our philosophy: Capital follows strategy and farmers goals, not the other way around.

What NZAB Capital does is broaden the range of capital solutions available to farmers when timing, leverage, speed, transitional periods, or structure mean a traditional bank may not currently be able to support a strategy in full.

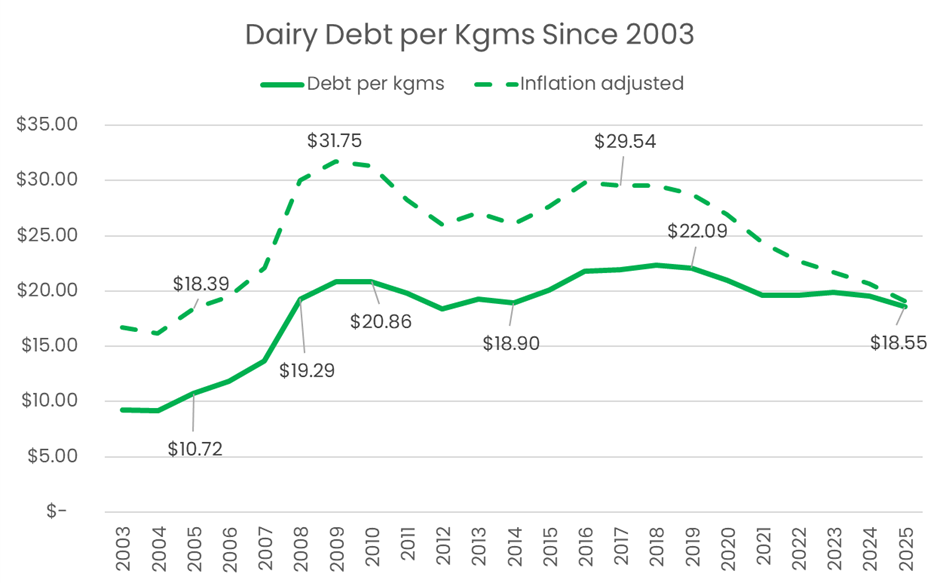

That growth in demand since launch has reinforced something we already suspected - New Zealand agriculture is increasingly requiring a wider range of capital options sitting alongside the traditional banking system.

In many ways, this is the re-emergence of genuine non bank agricultural lending in New Zealand

What is a non-bank lender?

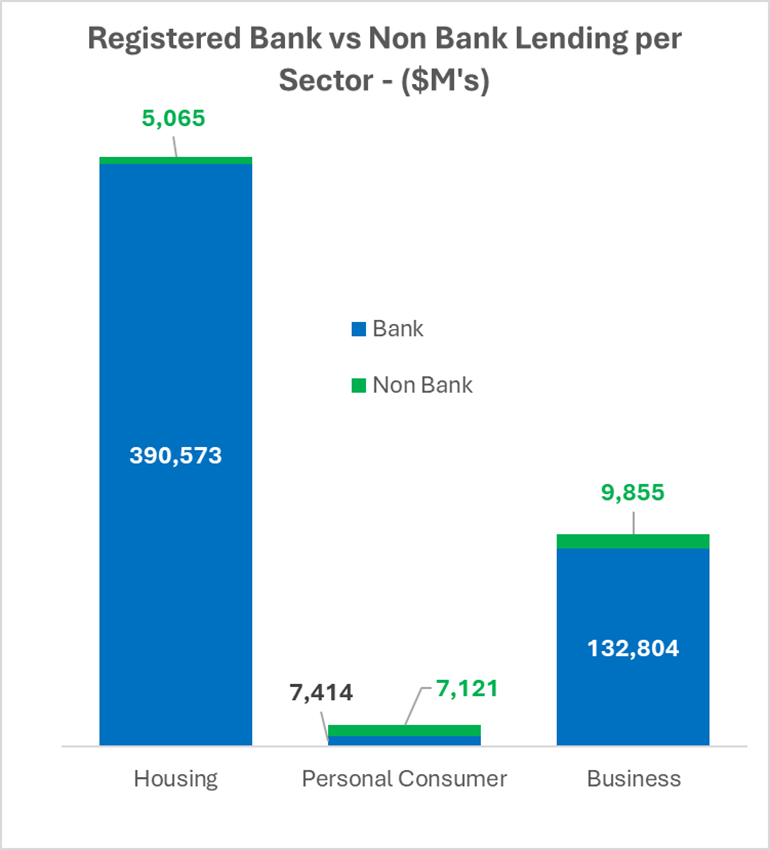

Non-bank lenders are already a very established part of the New Zealand financial system.

Most New Zealanders interact with non-bank lending regularly, even if they don’t realise it.

In residential housing, non-bank lenders have become a significant part of the market, particularly for borrowers who are self-employed, have complex structures, require faster approvals, or sit outside standard bank criteria.

Non bank lending has become very notable in the commercial property and business sectors. Non-bank lenders now play a major role funding development projects, transitional property transactions, business acquisitions, bridging finance, and restructuring situations where traditional banks may be slower moving or more constrained by internal credit settings.

.png)