Information only disclaimer. The information and commentary in this email are provided for general information purposes only. We recommend the recipients seek financial advice about their circumstances from their adviser before making any financial or investment decision or taking any action.

We all want to pay the lowest interest rate possible. It makes perfect sense. Two years ago our budgets had good allowances for principal and tax, but this year those amounts have all but rolled into the interest line.

Contrary to some opinions on this subject, I think that one of the greatest aspects of being a farm borrower is that you can get a rate based on how good you are, rather than a one size fits all rate like those buying a house. It gives you an element of control and brings in to focus the things that are important when you are presenting your business to a bank. The key is knowing how to access these benefits.

Rates are high again, and that's always when the question of fairness arises. They're not the highest they have been, but they are a lot higher than they have been for the last few years. To be honest we were pretty lucky that rates went as low as they did during the downturn in the dairy sector otherwise things would have been a lot worse for us as an industry. With the current challenges in the red meat sector, it makes sense to be looking hard at these costs.

So, what’s driving the increases?

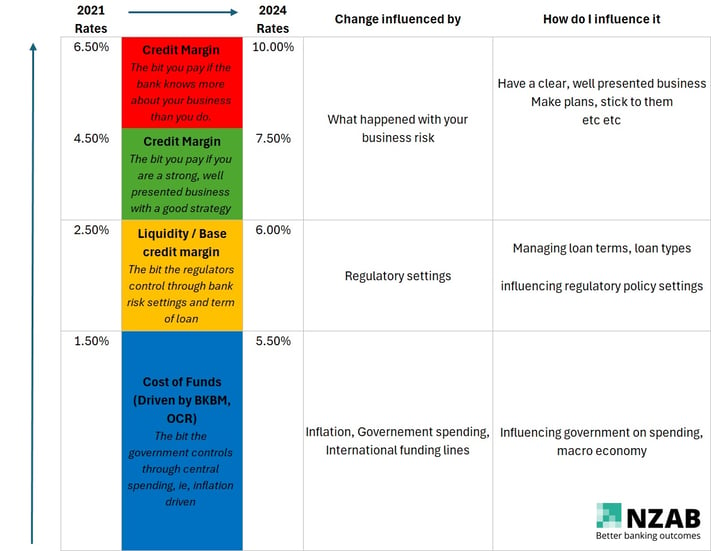

This is a (very) simple illustration of how interest rates have changed over the last few years. You can see where the components of the rate have changed, and how you much influence you as a borrower have over these changes.

It was heartening to hear Prime Minister Luxon talking about the role of government spending and inflation on the underlying cost of funds the other day, so at least at a macro level some of these factors are understood.

But the key message clearly has to be that a significant portion of the rate you pay is within your control. If you engage the right team around you, and can clearly articulate your business, you will get a better deal.

Competition is also a key driver here. We talk about the concept of 'creating a market' for your loan. This doesn't mean you have to shop around, but the banks know that their best clients could change, and that incentivises them to ensure that they don't have to change.

The rates in the table aren’t just an example, real farmers are getting the top end of those rates right now. You could too.

What about a commission of enquiry into rates?

A hot topic of conversation lately with the commission into retail rates going on. There are aspects of rural banking that I do think need greater scrutiny, and a formal enquiry might help level the playing field.

- Risk based pricing becomes the nail in the coffin when businesses hit genuine distress. Eventually the rates become so high that failure is all but guaranteed. Some banks are lenient here, most are not. When a business passes a certain threshold, I believe there needs to be a cap on rates, or even a commitment from banks to actually lower rates in order to genuinely help rehabilitate those businesses that need it. The difference could be funneled into principal or used to engage proper help to solve these issues.

- Risk appetite has become far too volatile. One of the biggest frustrations we have is when a business with a clear plan comes up against a change in bank appetite or strategic direction. How the banking sector assesses credit risk, and a genuine longer term approach to this is badly needed.

- The regulatory settings need a rethink. I’ve got no issue with a regulator wanting to protect the banking sector from failure, but we have to acknowledge that there is a genuine cost to the farmer for the bank holding more capital. The government has an opportunity to balance the current ‘bank centric’ focus on risk, and shift the thinking to more of a ‘farmer centric’ approach. This would reduce risk in the industry by keeping those margins with the farmers, but perhaps requiring minimum principal repayments in order for the bank to classify the loan as a lower risk grade. This would achieve the same overall result but do it by improving the position of the borrower rather than the bank.

Take home message:

Interest rates have become a complicated and highly subjective part of our farming businesses. If your rates have increased, and you don’t know why then you need to get people around you to help shed some light. There are gains to be made.

Oh, and remember, the rural bankers that live in our communities, grew up on our farms, went to our schools and are banking because they want to give back to an industry they love are not the enemy here.

It’s easy to say they are getting younger, and can’t make the same decisions they used to, but all of us started out that way at some point. Some of these tensions between regulator, bank and farmer are just as hard for the banker to navigate as they are for us, but I know for a fact that if we work together using facts and clear plans, we will get the right outcome.

Who is NZAB?

.jpg?width=540&height=360&name=NZABStaffGroups55%20(1).jpg)

Farming’s very complex and you can’t be an expert in everything. That’s why the best farmers gather a specialist team around them. Our specialty is better banking outcomes for our clients.

There’s no one better to work alongside you and your bank. With a deep understanding of your operation and our considerable banking expertise, we can give you the confidence and control to do what you do best.

We’ve been operating for over five years now and we’re right across New Zealand, For an introductory no cost chat, pick up the phone and talk directly to one of our specialists on 0800 NZAB 12.

Or if you prefer, Visit us at our website or email us directly on info@nzab.co.nz