In the past there were two key ways to get the best interest rate. Firstly, borrow lots of money, or secondly shop around. Debt was readily available, banks had appetite to grow, and we were going through a wave of land use change and intensification that allowed for lots of money to be lent out on as yet unproven scenarios.

Bank margins were low, liquidity cost was non existent, and competition was strong. Even 0.10% felt like a big gap even though interest rates were north of 7% for a long time!

Fast forward to today, and a lot has changed. We've been through a couple of global shocks, we've had increased regulatory intervention, we've got an agri banking sector that now needs to see commercial level returns. As a result of this, lending appetite is pretty flat. All of these factors have emboldened the banks to lift margins, have tougher conversations with their clients, and ultimately be less concerned about whether a client stays or goes.

So cheap debt is gone?

Nope. Rates are at historically low levels, you're probably paying a lot less than you were 5 years ago, but the range is now huge. At NZAB we deal with a large chunk of NZ Agri Lending, and we see rates on a daily basis between 3% - 6%. 'Risk Based' pricing is being adhered to in most cases. So what do you do?

You need to know how the bank views your risk!

Many farmers are unaware of the drivers of their interest rate and how to manage these. That can have a huge impact on the bottom line.

How big an impact?

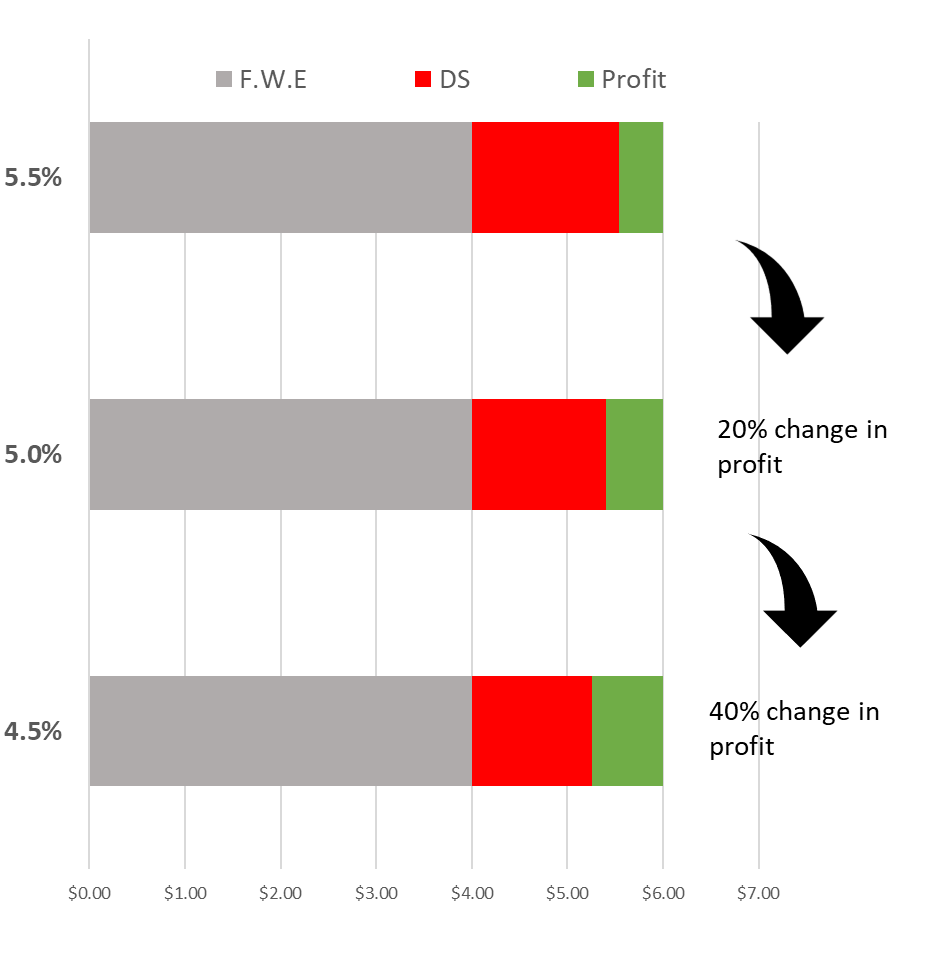

A change in interest rates causes one of the single biggest impacts on profit, positive or negative, and the example below illustrates this.

This bar graph looks at a typical (Average Debt) dairy farm, with the same cost structure and same level of debt in each scenario, but at different interest rates. With each increase or decrease in interest rate, by just 0.5%, that translates to an impact on profit of more than 20%.

To put this in context:

It’s the same as producing an extra 200kg of milk solids per hectare on a dairy farm, or on a cropping farm it’s the equivalent of growing an extra 1.5T of wheat per hectare.

Is that easy to do?

Given the significant impact on profit of such a small change, how much of your interest rate outcome is left to chance?

You can get what you deserve, but you can't do it without understanding why you aren't already getting the best deal. You also can't do it with out being prepared to make positive changes for the long term!

Ask yourself:

What have my recent meetings with the bank been like? Are they asking me what I want to do, or are they telling me what they need me to do?

Am I presenting a plan to the bank that I know can be met? Do I know what I will do if things change? Can I actually stick to it?

Do I know what the key parameters are that my bank look for and how I stack up against these?

Do I have a business with high enough quality where I could bank anywhere I want to?

Am I actually presenting all of this to the bank in a way that they understand, and leaves nothing to chance?

Challenging questions I know, especially because you're most likely not a farmer because you like banking..

You don’t need to be experts in this area, but you do need experts in this area!

We make it our mission to get what farmers deserve. Let us do what we do best so you can keep your time and energy focused on what you do best.