Last week I was fortunate enough to have a week off with the family and we thought we’d do our bit for the South Island tourism sector. Although this meant a different thing to our three girls who thought that retail therapy was their part in the revival!

We went to Queenstown for a few nights before hopping over to Doubtful Sound for an overnight trip and then onto Milford sound for a similar experience. Queenstown was nicely busy (without being frantic) and the tills and restaurants were ringing.

However it was a much different experience in Te Anau and Fiordland where the customer numbers were clearly a shadow of their former selves. Whilst it was nice to have more space, it did fell a bit eerie at times. If you get a chance, get out and spread the business around NZ, you will not be disappointed!

After I got back, it got me thinking about the different pain points that will evolve in our banking sector over the next period in Agri versus non-Agri commercial businesses

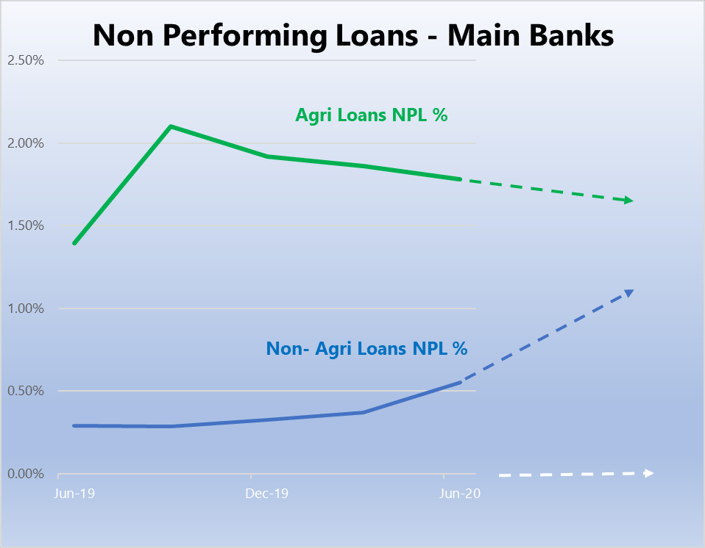

Recent RBNZ released data for the June 20 quarter gives us some insight into that changing pain, and in particular the change in non-performing loans.

If you recall, from our previous articles, Non-performing loans (“NPL’s”) are loans that the bank believes might have an issue with currently, or will in the future. It doesn’t mean that number will be their actual losses, but it is a trend line for where credit quality is heading.

Overall, Agri NPL’s continue to track favourably after a big lift last June 2019.

This is unsurprising – Agri businesses have in general performed very well over the last 12 months and current profitability still looks very favourable, albeit slightly lower than last year. They have also reduced significant debt- c. $1.2bn in the last 12 months alone.

Contrast that with the stark run up in Non Agri-NPL’s (and keep in mind, these also include housing loans which always attract less losses) – now trending upwards

This might play out two ways in terms of credit availability:

- Credit overall gets tighter, regardless of sector. Overall, NPL’s are going up, that means that banks' will become much more wary overall of all lending. This is quite feasible and some bank’s will definitely take this cautious approach.

- Agri lending credit quality continues to improve (and continues to get better relative to other sectors) making Agri Lending relatively attractive. This might lead to a more expansionary risk appetite (albeit still cautious) in the Agri Sector.

We think the latter may occur and are already seeing the green shoots of this amongst the banking sector, albeit not across all banks. Of note, some banks have been audible with; “repayments are happening faster than we thought” and “credit ratings are improving across the portfolio” and “we are keen to see more transactions”

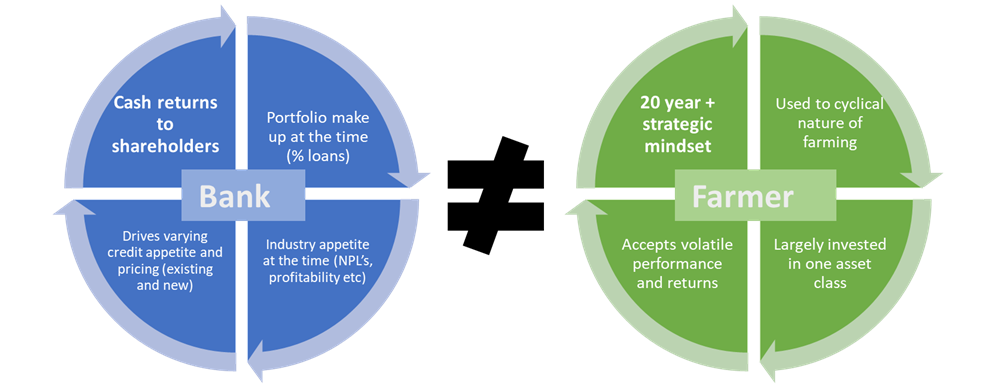

And this is where a gentle reminder comes in about the disconnect between bank growth strategy (or conversely, retrenchment) and your on-farm strategy.

Put simply, this means that the relative keenness of a bank to fund (or not fund) your next project may not just be about the merits of your on farm strategy and performance. In other words, just because the bank thinks it’s a good/bad idea does not make it a good/bad idea.

Independence in your decision making is critical here and an understanding of the bank portfolio dynamics in behind their thinking are essential before you make any large capital decisions

And which bank is going to be more or less available for farmers to fund?

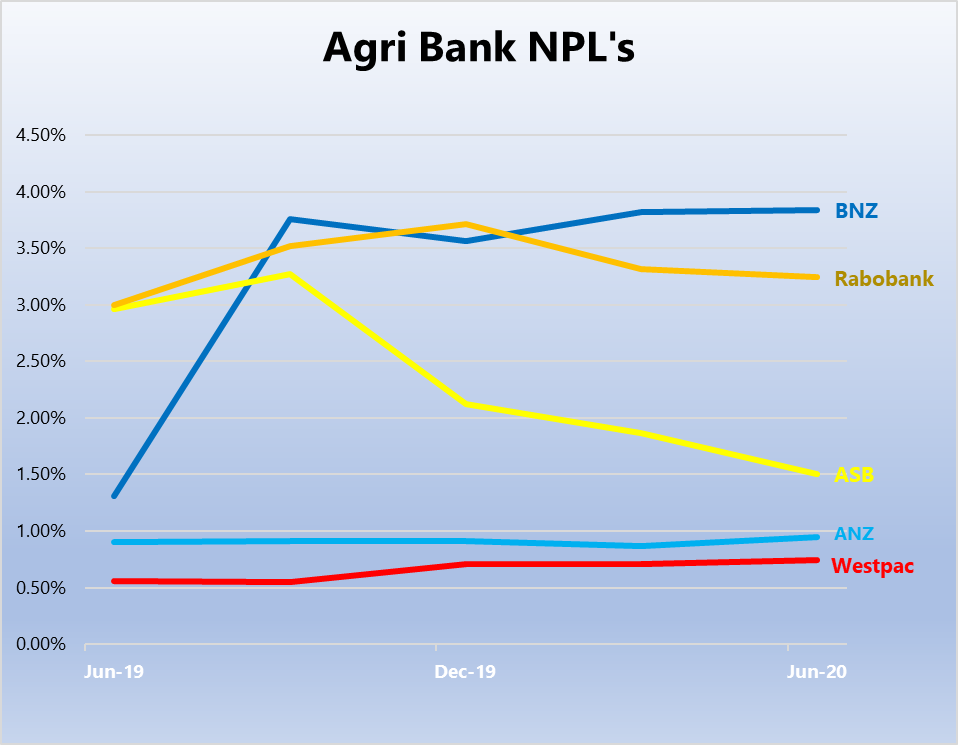

The next graph is one such data point:

BUT keep in mind, the above graph is but one data point– others which need to be taken into account are:

- A bank’s Agri loans as a % of their overall loans

- Agri loan return on equity (a function of the credit quality of their book and their current pricing +acquisition strategy)

- Parent bank (in Australia) Agri market share.

These all affect the appetite of your bank. NZAB is developing a market index to assist our customers with understanding the various bank appetite's at any one time. Look out for this in the future.

Increasing debt to a sector is not a bad thing.

Done properly and based around increasing efficiency (profit, productivity, better ESG outcomes), increased capital availability is a great thing as it generally increases the GDP of that sector – more jobs, more profits, more taxes and more investment into community good activities.

As always, if you want to have a chat with any one of our Client Directors, please sing out – we’d love to hear from you and talk about how we might help your business strengthen, grow and attract the best credit terms available.